Technology to Support Employee Movement and Work Location Flexibility

Managed international assignees, business travelers, and remote workers in one platform. Get the right people to the right place, compliantly.

Cross-border complexity, simplified

From quick business trips to long-term moves, Topia handles the compliance checks, documents, and audit trail in one place, so you can focus on moving people, not chasing paperwork.

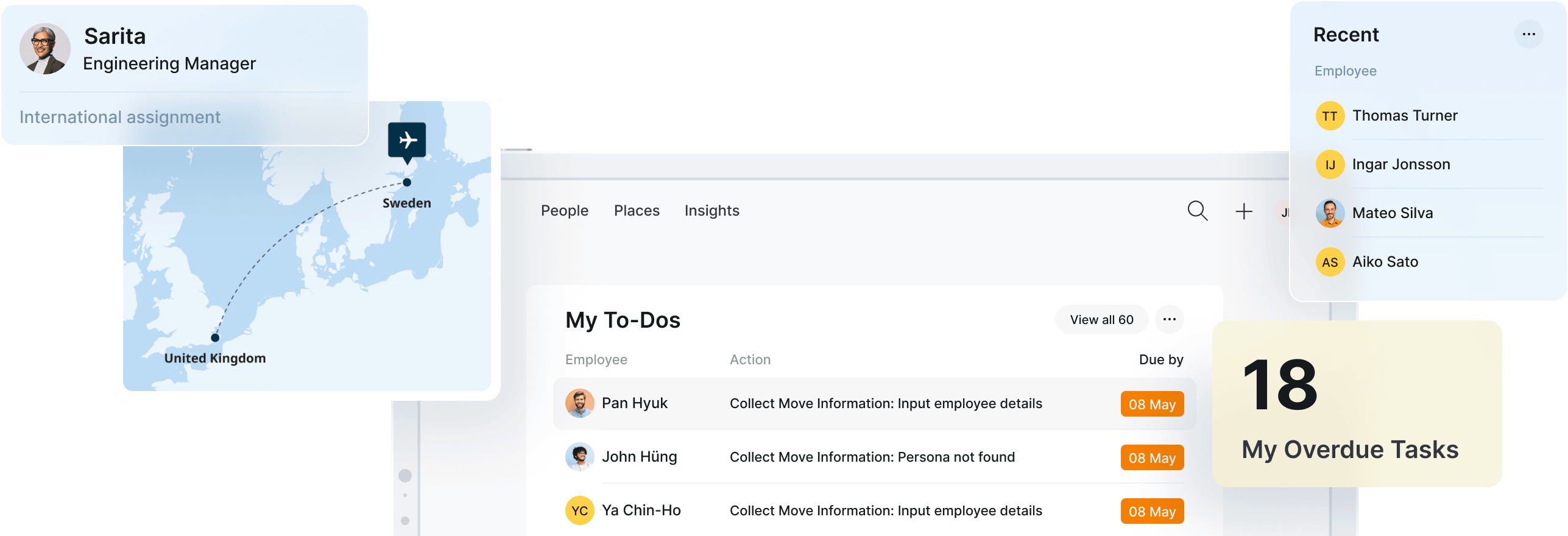

Move people across borders with confidence

From the first cost estimate to repatriation, keep every relocation on track in one workspace. Model packages, build balance sheets, and keep HR, Finance, and the employee aligned every step of the way.

- Cost estimates and balance sheets in a few clicks

- Pre-assessment for tax, immigration, and policy fit

- End-to-end tracking from kickoff to return

Relocations

Compliance check

What is Topia?

Topia is a global mobility platform that helps enterprises manage international assignments, business travel, remote work, and cross-border compliance in one unified system. HR, Finance, and Legal teams use Topia to automate tax compliance, immigration tracking, cost estimation, and workforce planning across 190+ countries.

Founded in 2010, Topia replaces fragmented spreadsheets and disconnected point solutions with a single source of truth for every employee on the move, from initial assignment through repatriation.

How Topia Works

Automate

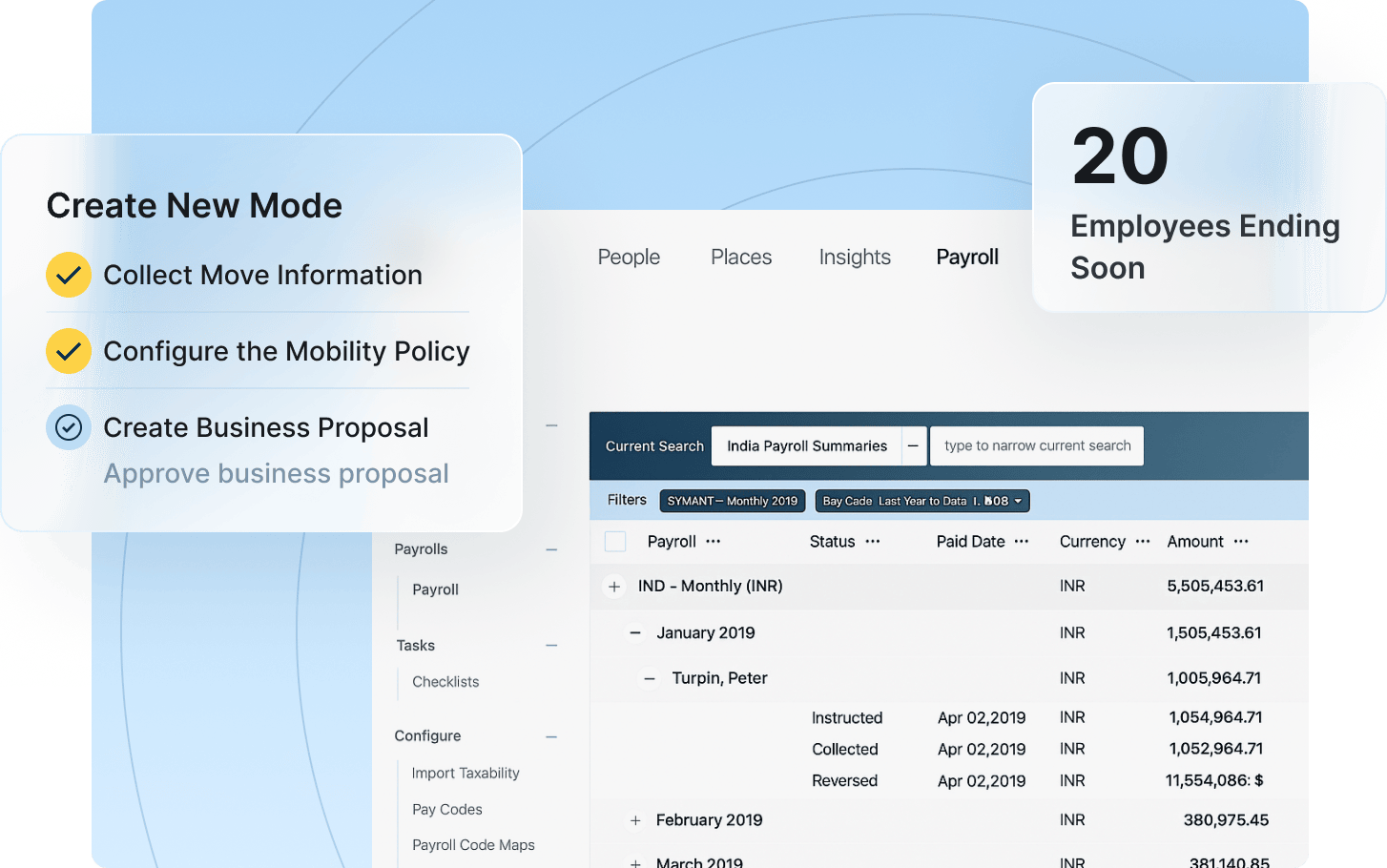

Key processes for global mobility and distributed work

- Save time and cut costs

- Increase efficiency across HR, Finance and Tax

- Simplify vendor management

Centralize

Resources, documents, and key mobility insights

- Smarter planning and cost forecasting

- Seamless cross-team collaboration

- One hub for every assignment, move, or trip

Visualize

Your workforce location and moving employee status

- Mitigate tax, immigration, and labor law risk

- Improve employee experience and retention

- Enable better, faster decision-making across functions

Why Topia?

Leading enterprises choose Topia to streamline processes, strengthen compliance, and support employees across every move.

Enterprise-Grade Compliance

Unify compliance and location management in one platform. From cost projections to vendor coordination, simplify every step of mobility management.

- Tax, immigration, and policy checks in one workflow

- Threshold alerts before limits are breached

- Audit-ready records for every move

A Global Community of Customers

From Fortune 100 enterprises to fast-growing, distributed companies, Topia scales with you, no matter your size, industry, or global footprint.

Our Clients

See how leading enterprises use Topia to streamline mobility and stay compliant.

"Topia has revolutionized our Global Mobility processes, greatly enhancing the experience of our internal stakeholders. Their feedback has been overwhelmingly positive."

Frequently Asked Questions

Everything you need to know about Topia, our platform, and how we help companies manage global mobility.

What is Topia?

Topia is a global mobility platform that helps enterprise, mid-market, and project-based organizations manage international assignments, business travel, remote work, and cross-border compliance in one unified system. HR, Finance, and Legal teams use Topia to automate tax compliance, immigration tracking, cost estimation, and workforce planning across 190+ countries.

What does Topia do?

Topia replaces fragmented spreadsheets and disconnected point solutions with a single source of truth for every employee on the move. The platform automates the full global mobility lifecycle, from initial assignment planning through repatriation, covering scenario-based planning, expat payroll, tax and immigration compliance, work location tracking, and reporting.

Who uses Topia?

Topia serves enterprise HR, Mobility, Finance, Payroll, Legal, and Compliance teams managing distributed workforces. Customers range from Fortune 100 enterprises to fast-growing distributed companies. Leading brands using Topia include Schneider Electric, Dell, Veolia, Equinor, AXA, ASML, Publicis Groupe, H&M, AIG, and Novartis.

What solutions does Topia offer?

Topia covers three core areas: business travel and work location compliance, remote and hybrid work, and global talent mobility. Specific solutions include pre-travel risk assessment, travel and work location tracking, remote work management, workforce mobility management, global mobility payroll instructions, and a global immigration library covering 70+ countries.

How does Topia handle immigration compliance?

Topia aligns destination rules with employee nationality, purpose of travel, and duration to flag immigration risks before travel begins. The platform continuously monitors work locations, triggers threshold alerts when compliance limits approach, and streamlines case workflows from feasibility checks through document expiry tracking and automated renewal alerts.

Does Topia integrate with existing HR and payroll systems?

Yes. Topia connects directly with leading HRIS, payroll, travel, and expense systems including ADP, SAP, Workday, Oracle, Ceridian, SAP Concur, and BCD Travel. The platform also delivers configurable flat-file instructions to any payroll provider, keeping data accurate across the global mobility ecosystem without duplicating effort.

How long has Topia been in business?

Topia was founded in 2010 and is headquartered in Denver, Colorado. In June 2025, Bow River Capital's Software Growth Equity team completed a majority recapitalization of Topia, accelerating the company's go-to-market strategy and product development roadmap. Topia operates globally with offices throughout the Americas and EMEA.

What is Topia Horizon?

Topia Horizon is the next-generation AI-driven platform built on Topia's global mobility foundation. Horizon adds agentic AI to case management, cost modeling, compliance, payroll, and policy in a single workspace. Built for mobility teams ready to move from reactive administration to proactive, intelligence-driven strategy. Learn more on the Horizon page.

Unlock Your Workforce's Global Potential

Flexible work solutions that drive productivity, visibility, and compliance.